Superb businesses

Smart capital allocation

We are all looking for companies that create shareholder value. In this post I will do a small case study of two companies. The idea will be to highlight what makes for a superb value creator and what makes for an also ran.

We can start with the idea that superb businesses generate far more cash than they can use internally. The value of this cash to shareholders depends on how effectively this cash is deployed by management – capital allocation.

As Warren Buffett puts it: “Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return.” (Buffett W. E., The Essays of Warren Buffett: Lessons for Corporate America. 1998) p.86. These are what Buffett calls the seven footers.

Predicting the future

In looking for a superb business the ultimate question is whether it is a business whose earnings are virtually certain to be materially higher five, ten and twenty years from now. I call this the Warren Buffett question. You can’t answer it by simply extrapolating recent performance.

The answer to this question is always a combination of understanding the company’s business franchise, its competitive position, its ability to generate sustainable free cash flow and its ability to reinvest that cash at high rates of return.

Let’s look at two companies and try to answer the Warren Buffett question for each.

A superb company

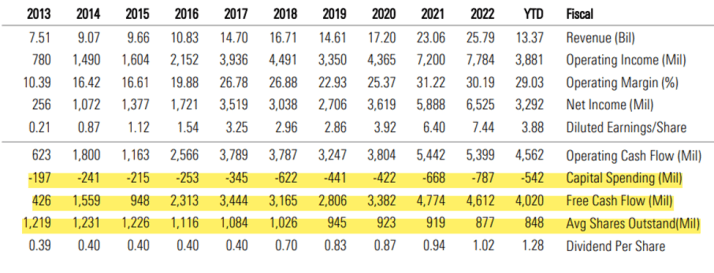

Applied Materials is the leader in materials engineering solutions used to produce virtually every new chip and advanced display in the world. Its expertise in modifying materials at atomic levels and on an industrial scale enables customers to transform possibilities into reality. The current board and executive officers hold about $1 B USD common shares. Market cap $100 B USD. My position was initiated in the spring of 2020 when it could be bought at a very attractive price.

Before you run out and buy shares in the company, be warned that the stock is currently significantly overpriced. Our purpose today is solely to answer the Warren Buffett question noted above.

Applied Materials operates in a growth area – technology. It is the largest vendor of semiconductor fabrication tools globally.

I have highlighted in yellow the numbers we need to look at. Over the last ten years its operating cash flow has vastly exceeded its capital spending, leaving it regular and growing free cash flow. Return on invested capital has exceeded 20% since 2017. It is clear from these numbers that the company’s capital spending is producing high rates of return. It is producing enough free cash flow on a sustainable basis that it has been able to consistently buy back shares over the years and reduce its share count and pay a growing dividend. This suggests quite strongly that the company has a wide moat and that management have been making smart capital allocation decisions.

Applied Materials Inc AMATNASDAQ/US

Source: Morningstar

An also ran

BCE is the biggest Canadian broadband provider, with over 4 million high-speed internet customers at the end of 2022 and a footprint that reaches 75% of the nation’s population. Its name used to be Bell Canada Enterprises. It is Canada’s Ma Bell. BCE also has the highest-quality and most diversified media unit of Canadian telecom firms, with Crave is BCE’s over-the-top video-on-demand service, HBO, Showtime, and Starz, Canada’s top network (CTV) and top sports station (TSN), 30 television channels, over 100 radio stations, an out-of-home advertising business, and broadcast rights for a multitude of sports teams, leagues, and events. It is a Canadian household name. It is a member of a telcom/media oligopoly in Canada. As such, BCE has a wide moat.

BCE has a market cap of about 40B USD. All the numbers below are in Canadian dollars. One Canadian dollar is worth about 73 cents USD. Its officers and directors own less than 1% of the company’s shares. Its current dividend yield is 6.5%. I have never owned any shares in the company.

Looking at the yellow highlighted numbers below, it can be seen that in recent years BCE has incurred between $4B and $5B in capital spending. Free cash flow shows as averaging over $3B annually recently. But the free cash flow is totally adsorbed by dividend payments. In 2022 the 912M shares outstanding received $3.68 per share for a total of over $3B. The number of shares outstanding are steadily increasing. Existing shareholders are being diluted. The company’s return on invested capital (ROIC) is in single digits and has been declining for ten years.

I think I can say with some certainty that this is a business whose earnings are virtually certain to be higher five, ten and twenty years from now. Whether they will be materially higher, even beating inflation, is open to question.

The stock is widely held in Canada and is a quintessential dividend stock. No investment advisor could be criticized for putting an unknowing client in the stock. A sell side analyst’s report says: “With a scale advantage, BCE consistently delivers an attractive balance of growth and profitability while continuing to make significant investments to future-proof the business and returning excess capital to shareholders through annual dividend growth.”

I couldn’t disagree more. The problem for BCE is that it has no avenues to invest excess capital at high rates of return. Its return on invested capital is abysmal. All its cash flow is needed either to maintain its existing business or to pay a substantial dividend.

BCE Inc BCETSX/CA

Source: Morningstar

Conclusion

I’ve chosen these two companies to illustrate how we can take a table of data and address the Buffett Question posed at the beginning of this post. It isn’t necessary to do a detailed statistical analysis. Inspection of the data shows quite clearly whether the companies have the business franchise to allow management to reinvest excess capital at high rates of return. Ten years of data are especially useful for this task. Companies will often have lumpy results from one year to another. The ten year numbers make the picture relatively clear.

+++++++++++++++

You can reach me by email at rodney@investingmotherlode.com

I’m also on Twitter @rodneylksmith

+++++++++++++++

Check out the Tags Index on the right side of the Home page that goes from ‘accounting goodwill’ to ‘wisdom of crowds’. This will give readers access to a host of useful topics.

+++++++++++++++

You can also use the word search feature on the right-hand side of this page to find references in both blog posts and also in the Motherlode.

+++++++++++++++

There is also a Table of Contents for the whole Motherlode when you click on the Motherlode tab.

Want to dig deeper into the principles behind successful investing?

Click here for the Motherlode – introduction.

If you like this blog, tell your friends about it

And don’t hesitate to provide comments or share on Twitter and Facebook

4 thoughts on “How to distinguish a superb value creator from an also ran”