Superb companies

Accounting practices largely ignore intangibles

One of the most misunderstood things in investing today is the way accounting and financial statements deal with (or don’t deal with) company investments in intangibles.

As much as we have read about this, it’s amazing how analysts and investors cling to distorted measures such ROC, ROIC, ROE, P/E and P/B. It’s not that these measures are meaningless. It’s that they are misleading. The key inputs for these measures are reported earnings and the book value of equity. It’s just that these inputs don’t mean what they used to, even ten years ago.

Do we know what’s happening?

I’m sure you have read about the massive shift by companies away from spending on tangible assets to spending on intangibles of lasting value (intangible assets). The accounting rules create an asymmetry in how they deal with this spending. It is only getting worse as the years go by. Companies that acquire intangible assets through corporate acquisitions treat those intangible assets as assets that appear on balance sheets. Companies that create intangible assets internally are, with certain limited exceptions, required to expense the related cash outlays. This is the asymmetry. As a result, the cost of creating major long-lived corporate assets ends up reducing net or reported earnings while, at the same time, creating long-lived intangible assets that do not appear on the balance sheet.

Capitalism without Capital

The book that hit me between the eyes on this is a highly stimulating work by Jonathan Haskel, a professor of economics at Imperial College London and Stan Westlake , a senior fellow at Nasta, the UK’s national foundation for innovation titled Capitalism without Capital, the Rise of the Intangible Economy (Haskel & Westlake, 2018).

Eric Hazen in a note November 12, 2021 for the McKinsey Global Institute wrote:

“Recent McKinsey Global Institute (MGI) research found that, by 2019, intangibles accounted for 40% of all investment in the United States and ten European economies, up 29% from 1995. And intangibles investment appears to have surged again in 2020 as digitalization accelerated in response to the COVID-19 pandemic.

We believe that this trend strongly hints at the emergence of a new model of capitalism, in which companies’ success will be measured more by their people and their capabilities than by their machines, products, or services. Moreover, we think there is no going back. Firms such as Amazon, Apple, Facebook, and Microsoft are clearly scaling up dramatically and achieving hyper growth.” For article see here.

As Kai Wu of Sparkline Capital has noted in a fascinating report titled ‘The Platform Economy’:

“Despite their rise, financial accounting practices largely ignore intangible assets. This omission leads investors to systematically undervalue intangible-rich companies. We believe this is the primary reason for the broad-based outperformance of platform companies we saw earlier.

Moreover, this leads traditional quant value strategies to struggle with platform companies. The companies with the strongest network effects tend to look the most expensive on metrics such as price-to-book or price-to-sales.” (emphasis added) For note see here.

Unaccounted for

As I have pointed out, it’s not just intangible assets that aren’t accounted for. It’s that reported earnings are artificially depressed by company investment in intangibles of lasting value, i.e. intangibles that are effectively assets. So, financial reporting and accounting practices are failing us.

Haskel and Westlake cite the work of Lev and Gu in looking at the question of whether a significant amount of intangible assets are ‘hidden from view, that is, not reflected on companies’ balance sheets. Their conclusion is that a great deal of internally generated intangible assets are indeed unaccounted for in companies’ financial statements. It appears many intangible investments, such as design, are allocated by accounting rules to selling, general and administrative expenses thus not being capitalized and expensed over their useful life.

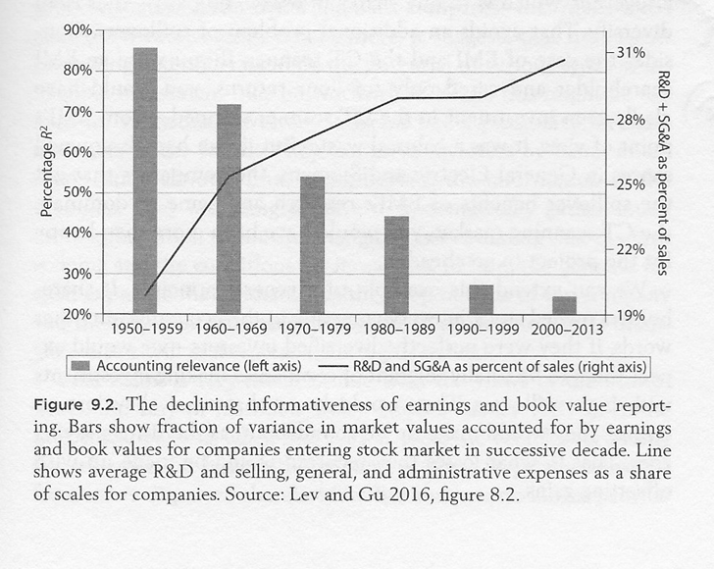

A noble effort to show on a graph

Haskel and Westlake have included a graph that attempts to quantify what they call the declining informativeness of earnings and book value reporting regarding intangibles drawn on the work of Lev and Gu. It is a depressing story.

Declining informativeness of earnings and book value reporting

And it is only getting worse.

What it all means for investors

The first step for investors is to come to a new understanding of reported earnings and the book value of equity. It also means that other measures, for example, ROIC become distorted.

We are all looking for companies that produce high returns on invested capital, well in excess of their cost of capital. And we want them to have the ability to reinvest that money at high rates of return. The first problem is that the ‘R’ in ROIC is either reported earnings or NOPAT or EBIT or some such. And of course, this number is distorted by company investment in intangibles of lasting value that are expensed against reported earnings.

The second problem is that the ‘IC’ in ROIC is based on the book value of equity. If massive investment in long lasting intangibles is not recorded in the book value of equity, the number for ROIC can be artificially high and unduly flattering to management and lead investors to believe that companies are generating higher returns on invested capital than is really the case.

The same distortion happens with ROC, ROCE, ROE, price earnings ratio (p/e) and price to book value ratio (p/b).

The solution

Some advocate for adjusting the earnings numbers and asset numbers to account for intangibles. I think this creates more trouble than it is worth. I prefer to focus on cash and the company cash flow statement. We want to find companies that are compounding free cash flow per share. The main problem, even with this approach, is that some great companies, in their growth phase, have negative cash flow for years. So you have to make a subjective judgement as to which of those companies is going to be able to convert that intangible investment into future compounding free cash flow.

Conclusion

Investing is not easy.

+++++++++++++++

For readers interested to dig deeper into these issues, take a look at these posts:

Heart of stock valuation: subtleties of free cash flow

Financial strength – the debt equity ratio has serious shortcomings

The fading usefulness of book value

Is the price earnings ratio (P/E) obsolete?

What is the right price earnings ratio?

The under-performance of value stocks explained

+++++++++++++++

To read more generally about what we are looking for in companies to invest in, take a look at the Motherlode Chapter 35. Capital Structure, Strength and Economic Performance

This chapter contains the following Sections:

35.04 Accounting treatment of intangibles

35.05 Accounting Goodwill and Economic Goodwill

35.07 Understated tangible assets

35.09 General discussion of debt and debt equity ratios

35.10 Debt to equity ratio conclusion

35.12 Net long term debt to free cash flow

35.14 Net long term debt to NOPAT

35.15 Conclusion regarding coverage ratios

35.16 Measuring Economic Performance

35.20 Impact of expensing intangible investments

35.22 Potentially the bigger problem

35.23 True value of equity, ROC, ROIC and ROCE

35.25 Coming up with free cash flow yield

35.26 ROC and a company’s cost of capital

35.28 Some examples of weighted average cost of capital using CAPM

35.29 Does the use of CAPM make sense in calculation the cost of equity?

35.30 Can we replace CAPM in calculations of cost of equity capital?

35.31 Earnings yields and cost of capital

35.32 Banks and life insurance companies

35.35 Other measures of company performance – Profit margins

35.36 Ratios used by management

35.38 Comparing with cost of capital

+++++++++++++++

You can reach me by email at rodney@investingmotherlode.com

+++++++++++++++

Check out the Tags Index on the right side of the Home page that goes from ‘accounting goodwill’ to ‘wisdom of crowds’. This will give readers access to a host of useful topics.

+++++++++++++++

You can also use the word search feature on the right hand side of this page to find references in both blog posts and also in the Motherlode.

+++++++++++++++

There is also a Table of Contents for the whole Motherlode when you click on the Motherlode tab.

Want to dig deeper into the principles behind successful investing?

Click here for the Motherlode – introduction.

If you like this blog, tell your friends about it

And don’t hesitate to provide comments or share on Twitter and Facebook

12 thoughts on “The emergence of a new model of capitalism”